Wages garnished for unpaid tuition was the exact phrase I searched at 6:12 a.m., staring at a paycheck deposit that was lower than it should’ve been. Not “a little off.” Not “maybe taxes.” It looked like someone took a clean slice out of it.

I wasn’t dealing with federal student loans. This was a college tuition balance from a semester I stopped attending. I honestly believed it was still in “collections letters” territory. But the paycheck proved something else: wages garnished for unpaid tuition had already started, and it was happening through my employer.

If you’re in the U.S. and you’re seeing wages garnished for unpaid tuition on your paystub, you’re not at the warning stage anymore. You’re at enforcement. The key move now is to stop guessing and identify exactly which legal path produced the garnishment—because each path has a different “fastest way out.”

Start here if you need the “before garnishment” timeline (it explains how college debt often escalates):

This guide helps you map what likely happened before the paycheck deduction. If you moved, changed emails, or ignored mail that looked routine, that context matters now.

What This Usually Means in a College Tuition Case

In most states, a private creditor can’t garnish wages without some form of legal authorization (often a court judgment). Colleges typically don’t “garnish” wages directly. The common chain is: school account → collection agency → lawsuit (or court process) → judgment → wage garnishment.

The paycheck deduction usually means a judgment or court order is already in play. That’s why the first goal is not “argue your story” but “identify the case record and the basis for the garnishment.”

When wages garnished for unpaid tuition is already happening, your leverage comes from facts: service records, amounts, dates, court jurisdiction, state limits, and whether the debt is even yours or even accurate.

Identify Which Scenario You’re In

A) Default Judgment (Most Common)

You never responded to a lawsuit (often because you never saw it). The creditor won by default, then requested garnishment.

B) You Were Served, But Missed the Court Date

You did get papers, but assumed it was “a collection threat,” missed deadlines, and judgment was entered.

C) Stipulated Judgment / Payment Agreement

You signed something to “avoid court,” then missed a payment. Some agreements include enforcement language.

D) Wrong Person / Identity Mix-Up

Similar name, old roommate, incorrect SSN association, or a debt transferred with errors. Rare, but real.

E) Amount Is Inflated or Incorrect

Fees, interest, “collection costs,” or tuition after withdrawal were added incorrectly, and the garnishment reflects a bad total.

F) Multi-Job or Irregular Income Confusion

Garnishment percentage is misapplied across jobs, or the employer calculated disposable earnings incorrectly.

Keep reading with the branch you picked in mind. The “right” response depends on that branch.

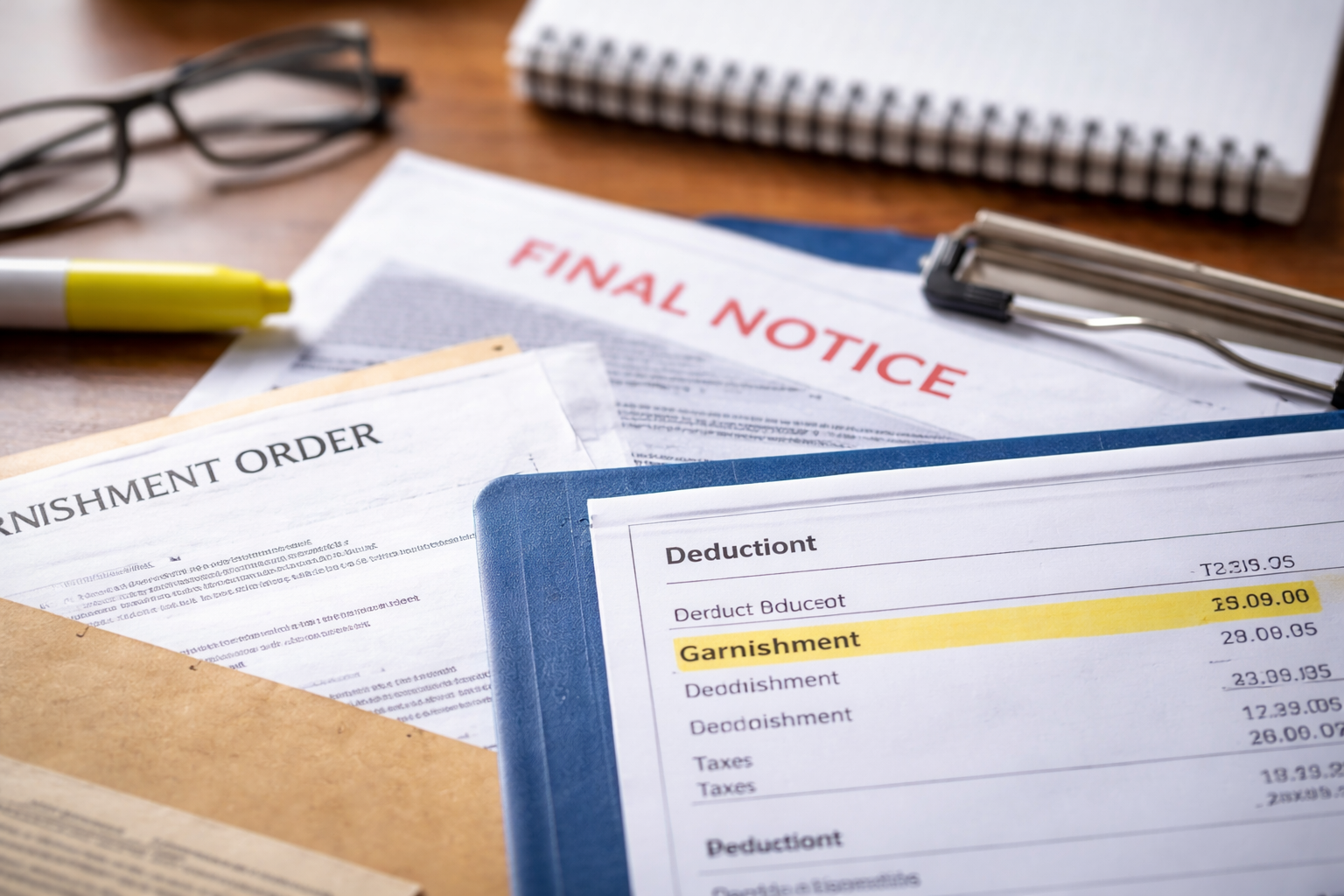

Fast Proof: The 4 Documents That Tell the Truth

When wages garnished for unpaid tuition hits, people often call the school first. That can waste days. The fastest clarity comes from four documents:

- 1) Your paystub detail (look for a garnishment code, case number, or agency name)

- 2) The “garnishment order” or “withholding order” your employer received

- 3) The court docket (the case file summary—dates, judgment amount, parties)

- 4) The judgment (the legal document authorizing enforcement)

If you can get the docket and judgment today, you stop operating in the dark. Most courts let you access docket info online, and the clerk can provide copies (fees vary).

If You Never Got Served: Your Best Chance to Reopen the Case

Branch A is common: you didn’t respond because you didn’t know you were sued. If wages garnished for unpaid tuition started and you truly never received service, you may have options such as a motion to vacate a default judgment (names vary by state).

What strengthens your position:

- You moved and the lawsuit was sent to an old address

- The service method doesn’t meet state rules (posted notice, incorrect person served, etc.)

- The court is in a county/state you didn’t live in (possible venue issue)

- You have proof the balance is wrong (withdrawal date, billing error, aid posting issue)

What weakens your position:

- You received certified mail/served papers and ignored them

- You previously acknowledged the debt in writing without disputing it

- You waited too long after learning about the judgment (deadlines vary)

Even if reopening the judgment is hard, raising “service issues” can improve settlement leverage. Creditors don’t love uncertainty.

If the Amount Looks Wrong: Audit the Tuition Timeline

Sometimes wages garnished for unpaid tuition is based on a total that doesn’t match your memory. That’s not a small detail—it’s your negotiation starting point.

Do a quick audit using these questions:

Self-Audit Checklist

- Did you withdraw officially, and what was the withdrawal effective date?

- Were you charged tuition after dropping classes or after a deadline?

- Did financial aid reverse and create a sudden balance?

- Are there “collection costs” added that you never agreed to?

- Does the judgment include attorney fees or interest that seems inflated?

Don’t argue in generalities like “I can’t pay.” Argue with line items. If your balance is overstated, that’s a concrete dispute point—especially if documentation exists.

Understand Garnishment Limits Without Turning This Into a Legal Lecture

There are limits on how much can be taken from “disposable earnings” in many situations. The practical point is simple: if wages garnished for unpaid tuition is taking an amount that seems too high, your employer’s calculation or the order may be wrong for your state or your circumstances.

One official reference point for wage garnishment basics is the U.S. Department of Labor (CPPA fact sheet):

If the deduction is crushing your essentials, verifying the percentage is not optional. A miscalculation can run for months if nobody challenges it.

The Exact Phone Script Changes by Scenario

A) Default Judgment / Service Problem

Goal: get case number, judgment date, service method, and ask for a settlement that pauses garnishment while you review vacate options.

Key phrase: “I’m reviewing service and court records. I’m prepared to discuss resolution if enforcement is paused during review.”

B) Amount Dispute

Goal: demand an itemized breakdown tied to the judgment and compare it to school billing records.

Key phrase: “I’m disputing the balance basis and requesting itemization of principal, fees, interest, and costs.”

C) Payment Agreement Default

Goal: renegotiate terms that replace garnishment with an automatic plan (lower friction for them, stability for you).

Key phrase: “I can maintain an auto-plan if garnishment is released upon first cleared payment.”

D) Wrong Person

Goal: immediate escalation; request validation and dispute identity.

Key phrase: “I dispute this debt belongs to me. I need validation and correction immediately.”

F) Multi-Job Calculation Issues

Goal: confirm disposable earnings calculation and whether multiple withholdings are stacking incorrectly.

Key phrase: “I need the withholding calculation method and confirmation it matches the order and state rules.”

That’s not “legal theater.” It’s you speaking in the only language that moves a collector: enforceable facts and specific asks.

Mid-Story Reality: Why Collectors Will Still Deal After Garnishment Starts

People assume wages garnished for unpaid tuition is a locked system. In reality, garnishment is slow, administrative, and annoying for everyone involved (including your employer). Many collectors would rather convert it into a settlement or payment plan that closes the file.

The key is to offer something realistic, structured, and fast:

- Option 1: A lump-sum settlement (often strongest leverage if you can do it)

- Option 2: A short-term plan (60–120 days) in exchange for releasing garnishment

- Option 3: A longer plan with autopay and a written “release upon X payments” term

Your goal is to replace unpredictable enforcement with predictable closure. That’s a win for both sides if done correctly.

If you want the “numbers and wording” playbook for negotiation, use this supporting page:

This one bridges the lawsuit stage to the enforcement stage and helps you avoid giving collectors free leverage in your wording.

What to Say to Your Employer (And What Not to Say)

Your employer is usually required to comply with a valid garnishment order. HR/payroll often can’t “stop it” on request. But they can provide crucial info: the name of the issuing court/agency, dates received, and the contact details attached to the order.

Say this:

- “Can you share the case number and the issuing entity on the order?”

- “When did payroll receive the withholding instructions?”

- “Is there a contact phone/address listed for the creditor or court?”

Do not say this:

- “I refuse this” (payroll can’t act on that)

- “I’ll quit if you don’t stop it” (hurts you, not the order)

- “This is illegal” (unless you can point to a specific defect)

Keep your employer relationship clean. Focus your fight where it belongs: the order and the creditor.

Avoid These Costly Mistakes When You’re Panicking

When wages garnished for unpaid tuition appears, panic creates predictable errors. These are the ones that usually make things worse:

- Making a partial payment without terms (it can be treated as acceptance without stopping garnishment)

- Talking too much on the phone (you can accidentally confirm details you should verify first)

- Agreeing to a plan you can’t maintain (default restarts enforcement and adds fees)

- Ignoring the court record (the docket is where the real leverage lives)

Paying “something” is not a strategy. Paying under a written release plan is a strategy.

FAQ

Can a private college garnish wages for tuition?

Typically the school (or a collector) must have a legal basis such as a judgment, and the process varies by state.

Can this happen without me ever seeing court papers?

Yes. Address changes, improper service, or missed mail can lead to default judgments. If wages garnished for unpaid tuition started and you never knew about the case, you should check service records.

Will the garnishment stop if I call the school?

Usually not. Once a collector or court process is involved, the school often cannot directly stop enforcement.

What if the balance is from a semester I didn’t complete?

That can still create tuition liability depending on withdrawal rules and deadlines. Focus on dates and billing records.

Is negotiation still possible after garnishment begins?

Often yes. wages garnished for unpaid tuition can sometimes be replaced by settlement or a payment plan if you negotiate correctly and get terms in writing.

Key Takeaways

- Wages garnished for unpaid tuition usually signals a judgment or court-authorized enforcement.

- Pull the docket and judgment first; don’t rely on phone explanations.

- Service problems, amount errors, and identity issues can change leverage fast.

- Collectors may still settle because garnishment is slow and administrative.

- Your strongest move is a written plan that replaces garnishment with predictable closure.

What to Do Today (In This Exact Order)

- Get the case number from payroll paperwork or the court docket.

- Request the judgment copy and confirm the judgment amount and date.

- Check service details (address, method, date). If you never got served, note that immediately.

- Decide your path: challenge (service/amount/identity) or negotiate settlement/plan.

- Call with purpose: ask for garnishment release terms in writing.

For the “next action” path—how to structure a realistic settlement offer and get the release language you need—use this:

When I saw the deduction, it felt like the decision had already been made without me. But that’s the trick of this stage: wages garnished for unpaid tuition makes it feel final even when there are still levers.

Do not wait for the “next paycheck” to confirm it’s real. Get the docket, get the judgment, and act today—either to correct the record or replace garnishment with a written settlement plan you can live with.