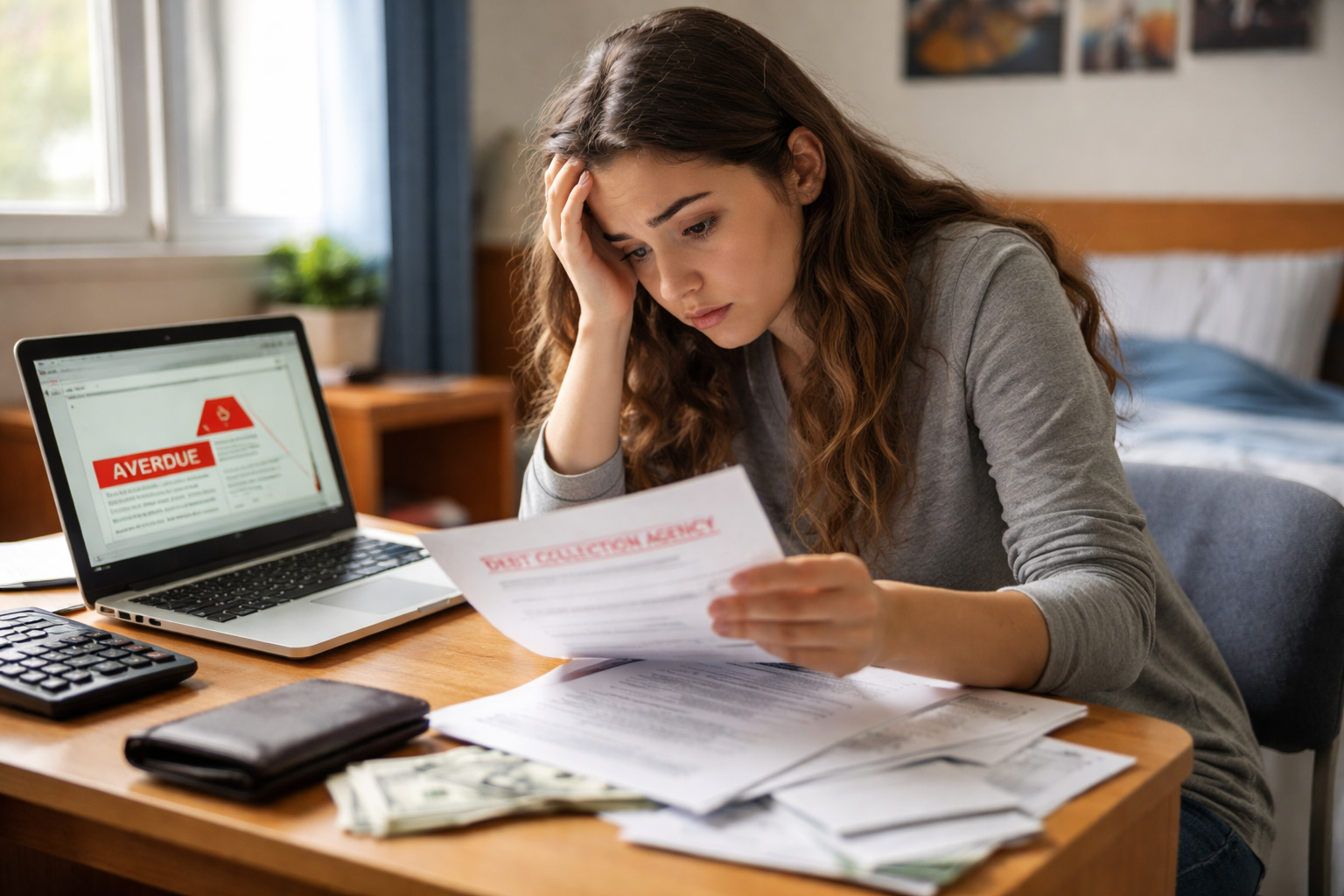

Bursar sent my account to collections without notice — that was the phrase I typed the second I opened a letter from a collection agency and saw my university’s name printed like it belonged there. I didn’t recognize the “account number” they referenced, but the amount was close enough to my last tuition statement that my stomach dropped.

I logged into the college billing portal expecting to see a big red overdue banner. Instead, the portal looked almost clean. The balance at the school level was lower than expected, and the only clue was a line item that said something like “Transferred.” When bursar sent my account to collections without notice, it didn’t feel like I missed a payment. It felt like something happened in the background and I was being notified last.

This guide is written for U.S. college and university billing situations. It is not legal advice. The goal is to help you take fast, practical steps that prevent credit damage, stop escalation, and force clarity from the school and the collector.

If you need the baseline explanation of how tuition debt typically moves into collections, start here (then come back):

Stop Guessing: The 3 Questions That Control Everything

Before you do anything emotional or irreversible, lock down these three facts. When bursar sent my account to collections without notice, these questions determine whether you should dispute, negotiate, or pay — and who you should pay.

- Was the debt sold or assigned? (Sold = collector owns it; Assigned = school still owns it.)

- Has it been reported to credit bureaus? (If not, you may still prevent reporting.)

- What is the school’s referral date? (This reveals whether notice procedures were followed.)

If you only take one action today: get written confirmation of these three points.

Why the Bursar Referred You “Without Notice”

When bursar sent my account to collections without notice, it almost always falls into an internal trigger. The school rarely frames it this way, but the mechanics are usually predictable.

Case A: Notice went to a dead address

• The school used your student email you no longer check.

• Mail went to an old address in the student information system.

• You opted out of paper billing and didn’t realize it.

Case B: Payment plan defaulted quietly

• One installment failed due to expired card or bank rejection.

• The plan auto-cancelled and the whole balance became due.

• Late fees posted, pushing you over the referral threshold.

Case C: Third-party payment failed (529, employer, sponsor)

• A sponsor promised payment but missed deadlines.

• A 529 distribution was delayed or coded incorrectly.

• The school treated it as your responsibility once past due.

Case D: Financial aid reversal created a retroactive balance

• Aid was adjusted after verification.

• Enrollment status changed (dropping below full-time).

• A grant was clawed back, creating a sudden balance.

Case E: Administrative charge posted after the term ended

• Housing, lab, technology, or health insurance fee posted late.

• A transcript or graduation fee appeared unexpectedly.

• The system treated it like an old delinquency.

Case F: You were never billed correctly until now

• The school discovered an undercharge and corrected it late.

• The “corrected” ledger triggered referral without a new notice cycle.

Even if bursar sent my account to collections without notice is “allowed” under the school’s terms, you can often challenge the process if you can show poor notice, unclear billing, or an error ledger.

What the College Will Say vs. What You Need in Writing

When you call the bursar and say bursar sent my account to collections without notice, you’ll often hear one of these:

- “We sent emails to your student account.”

- “This is automated after 90 days.”

- “You agreed to electronic communication.”

- “You need to speak to the agency now.”

Verbal explanations don’t protect you. Written records do.

Ask for these documents or screenshots:

- Full account ledger (every charge, credit, adjustment, and date)

- Referral date and referral policy section (their own handbook language)

- Proof of notice attempts (email logs, mailed statements, portal notices)

- Name of the collection agency and whether debt was sold or assigned

The 48-Hour Action Plan (Do This in Order)

When bursar sent my account to collections without notice, speed matters because credit reporting and added fees can start quickly. This is the cleanest order to prevent long-term damage.

Step 1: Get the bursar ledger in writing (PDF/email).

Step 2: Ask the school: “Was this debt sold or assigned?”

Step 3: Ask the agency: “Has this been reported to credit bureaus?”

Step 4: Send a written debt validation request to the agency.

Step 5: Request recall if the ledger shows an error or missing notice.

Do not pay the agency first if you haven’t confirmed whether paying the school directly is still possible. In many college cases, paying the school can trigger a recall or at least stop escalation.

Debt Validation: The One Step People Skip (And Regret)

If bursar sent my account to collections without notice, you may feel pressure to pay immediately to make it disappear. But the first smart move is validation — not because you’re trying to dodge a bill, but because you need to confirm the amount, dates, and authority.

What your validation request should ask for:

- The name of the original creditor (the college) and the account reference

- The exact amount claimed, including any fees

- The date of delinquency or referral

- Proof the agency has authority to collect

- How they handle credit reporting (if applicable)

Official consumer guidance on debt collection rights is available from the Federal Trade Commission:

Validation forces the conversation to be about documents, not pressure.

How to Tell If This Will Hit Your Credit

Not every tuition collection account appears on your credit report immediately. Some agencies report; others don’t. When bursar sent my account to collections without notice, you need clarity, not assumptions.

Ask the agency directly:

- “Do you report to credit bureaus?”

- “If yes, when is the earliest reporting date?”

- “If the balance is resolved, do you request deletion or update status?”

If you want a deeper breakdown of credit-report impact, use this internal guide:

When You Can Push for Recall (And When You Probably Can’t)

The most valuable outcome after bursar sent my account to collections without notice is recall — the school pulls the account back from the agency. Not always possible, but these conditions improve your odds:

- Ledger shows an error, duplicate charge, or late-posted fee with no notice cycle

- School cannot show reasonable notice attempts

- You can pay principal quickly or enter an approved payment plan

- The balance was triggered by a sponsor delay you can document

If you need a structured negotiation approach that protects you while you work the process, use:

Recall is more likely when you sound organized, prepared, and ready to resolve — not panicked.

If This Is Actually a System or Portal Issue

Sometimes bursar sent my account to collections without notice happens because the portal didn’t reflect a payment or posted an adjustment late. If you paid and the portal didn’t update, that’s a different track.

Use this internal guide if payment tracking is the trigger:

If you can prove payment timing, you can often force correction and possibly recall.

Mistakes That Make This Harder (Avoid These)

When bursar sent my account to collections without notice, these are the most damaging missteps:

- Ignoring the collector because you “never got notice”

- Paying immediately without confirming the debt status (sold vs assigned)

- Arguing by phone and leaving no paper trail

- Missing internal appeal deadlines

- Letting the school shift you entirely to the agency without requesting documentation

Your leverage is paperwork and timelines. Protect both.

FAQ

Can a college send my account to collections without notice?

Policies vary. Many schools rely on electronic notices and portal postings. The key is whether they followed their published process and whether you can document the lack of reasonable notice.

Should I pay the school or the collection agency?

First confirm whether the debt was sold or assigned. If assigned, paying the school may still be possible and can reduce escalation. If sold, you may need agency resolution.

Will this block my transcript or registration?

Often yes. Colleges frequently place holds when accounts are delinquent or referred. If you are blocked from enrollment for unrelated billing timing, compare:

What if this escalates to wage garnishment?

Garnishment typically requires additional legal steps. If you’re worried about escalation, read:

Key Takeaways

- Bursar sent my account to collections without notice often results from automated thresholds, plan defaults, or late-posted charges.

- Your first job is to confirm: sold vs assigned, reporting status, referral date.

- Debt validation is a protective step, not a delay tactic.

- Recall may be possible if notice or ledger accuracy is weak.

- Act within 48 hours to prevent fees and credit escalation.

When bursar sent my account to collections without notice, the worst part wasn’t the balance. It was how quickly the situation changed once a third party was involved. The school became harder to reach, the language got colder, and suddenly everything had a deadline.

If bursar sent my account to collections without notice in your college situation, act today. Get the ledger, demand written proof of referral and notice attempts, send a validation request, and push for recall if the timeline doesn’t add up. You’re not asking for special treatment — you’re asking the system to prove it followed its own rules.